Introduction

As a commercial collection agency, the primary way AG Adjustments (AGA) helps our clients is through the collection of their seriously delinquent debt. One of the ways that our clients can aid in our collection efforts is by having their customers fill out a credit application that provides measures of protection and will increase the ultimate collectability of an account. We cannot emphasize enough how many times we have been successful in the recovery of our client past due monies because of their proactive approach in obtaining a well-drawn up credit application.

As a company working in the B2B space the credit application is one of the primary tools available for controlling credit risk when extending credit to your customers and protecting your company. A credit application is a contract between the seller and the buyer. A good credit application will benefit the seller, a bad one the buyer. Therefore, it is important that your company be certain that your credit application, whether electronic or in paper form, contains all the safeguards and guarantees available to reduce customer risk. Securing a credit application, while certainly does not guarantee payment, is one of the more significant documents you can obtain in assisting in not only the credit decision but the ultimate collectability of your past due accounts receivable and collection fees. The adage that “the sale is not complete until the money is in the bank’ is as true today as ever. A good credit application will assist in getting your company to that point.

What Do You Need to Know to Control Credit Risk?

The credit application is your first step in gathering information about your potential customer. The more you know about them, the better off you are and the easier it will be to make a good decision and collect the necessary information to determine how much credit to extend them. You can never assume all the information on the application is correct and you will need to do your due diligence to help you verify the information provided you before you grant credit. Therefore, it is important that the sales department make sure that every customer fills out and signs the credit application prior to any goods or services being delivered.

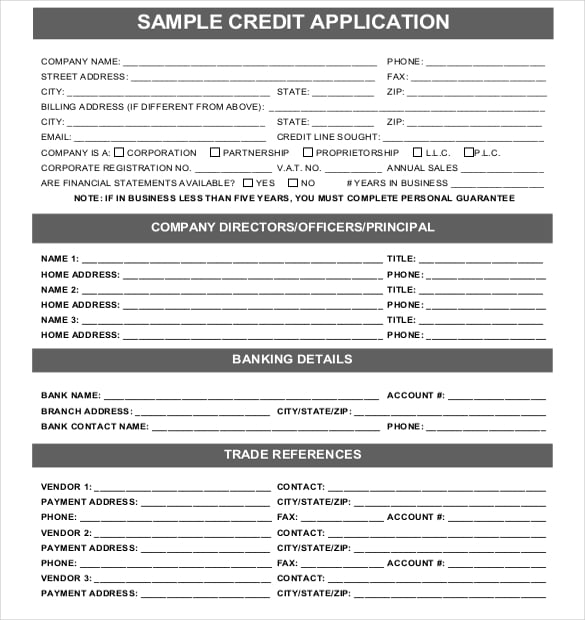

A typical credit application requires that at least the following information be provided:

• Name and address of the applicant

• Name and address of any parent company

• All contact information: I e: phone #’s, e-mail addresses etc.

• Type of entity (i.e., corporation, partnership, proprietorship, etc.)

• Names of principals/directors/officers

• Bank references

• Trade references -at least three

• Tax ID and DUNS number

• Availability of financial statements

• Credit limit requested

• Applicant’s agreement to payment terms

• Applicant’s agreement to interest on past-due amounts

• Applicant’s agreement to pay for legal and collection costs

• Applicant’s personal guaranty(s) with spouses if possible and authorization to pull personal credit report with SS#.

• Right to verify data on application from external sources (banks, trade references, credit bureaus, etc.)

• Signer(s) is an officer or authorized to bind the buyer

The Most Important Things to Consider

A credit application serves two purposes: It is a data gathering tool and it is a contract. As a contract, it specifies the rights and obligations of both the customer and creditor. As you are writing the application bear in mind that it’s a request for credit to be extended and should be written so that it provides your company an advantage if your business relationship fails. As we all know and “credit is not a right but a privilege”. The most important things to consider are:

• The signer(s) must be able to legally bind the company. If the signer is not authorized to accept the terms and conditions of the credit application, they can’t sign the application.

• If possible, make a personal guarantee part of your credit application. We would recommend that when extending credit to SMB’s that you get the owners and their spouses to sign a personal guarantee. While many personal guarantees have no value, it’s better to have one than to not and if a SMB owner is not willing to sign a personal guarantee, that might tell you something as well. You also want the social security number of the individual signing the personal guarantee so that if you must enforce it, you will have an easier time tracking them down in the event they abscond.

• You want a stipulation that the customer will pay interest on past-due amounts and will pay any collection, legal fees and court costs that are incurred because of non-payment. If you do not have this detailed in your credit application, you will NOT be able to collect fees on your debt if placed with a collection agency. In the event of litigation, it is up to the local courts jurisdiction if collection fees, attorney fees and interest will be awarded

• You want assurance that only the disputed portion of a past due amount will be withheld.

• If you file suit over non-payment, you want it to be as convenient as possible. The choice of venue must be yours. While many creditors will request suit in their local jurisdiction, this is not necessarily in a creditors best interest. The customer’s assets are normally local to their whereabouts. Therefore, in the event post judgment remedies are needed the judgment must be recorded in a debtor’s local jurisdiction to attach assets.

• You want authorization to obtain information from credit bureaus, banks and trade references both before authorizing credit and ongoing once they are a customer.

• You want current financials and the ability to obtain financials in the future once they are a customer

Verifying the Credit Application

Once you have the credit application in hand you need to verify the information it contains. At least three trade creditor references should be contacted as well as their banks to verify the existence of their checking account. You should be sure that all their references are legitimate. If for some reason you can’t contact one – be sure at least that they exist. Any false information on the credit application is a valid reason for not doing business. If the buyer is looking for a substantial credit line, make sure you review their financials, especially a statement of cash flow. If they are operating in a negative cash position you need to be sure that they will have enough cash available to pay you. Limit their credit line or at the very least change their terms if it looks that they may have a cash flow problem.

Once They Are a Customer

Periodic credit reviews are a necessity. Major account defaults can come from existing long-term customers as well as the new ones. Customer credit limits should be reviewed periodically, at a minimum once a year. Get current financials from your accounts annually if possible. Make sure their cash position can support their business. Additionally, obtaining current credit bureau reports on your largest customers, annually, is a good idea. Stay on top of your accounts receivable aging. If a customer is always 60 to 90 days past-due on some part of their balance, they are only one period away from being a problem.

A sample credit application can be found by following the link below:

https://images.template.net/wp-content/uploads/2016/05/07061009/Sample-Credit-Application.jpg

{kind=link}